Artificial Intelligence isn’t just reshaping how businesses operate – it’s reshaping where money flows. Over the past year, one investment theme has quietly moved from niche to necessity for major allocators: AI infrastructure funds.

These funds don’t invest in AI apps or speculative AI startups. Instead, they target the picks-and-shovels layer of the AI boom – the compute power and hardware required to train, deploy, and run modern models.

And this is where the story gets exciting: real yields, backed by real demand, driven by a global AI arms race.

Let’s break down what’s happening and why institutions are piling in.

Why AI Infrastructure Is Becoming a Core Asset Class

Modern AI requires staggering amounts of compute – especially GPUs, the chips optimized for parallel processing. Every major tech company, government, research lab, and enterprise upgrading its AI stack is competing for access to the same scarce resource.

This has created a new, fast-growing market: AI compute leasing.

Instead of buying GPUs outright, companies are renting access to GPU clusters hosted in specialized data centers. This is comparable to leasing industrial equipment – but the yields can be significantly higher.

Meanwhile, institutional investors (pension funds, endowments, sovereign funds, and insurers) are looking for:

– Hard-asset exposure

– Inflation-resistant cash flow

– Non-correlated returns

– Participation in the AI supercycle

AI infrastructure funds check all of those boxes.

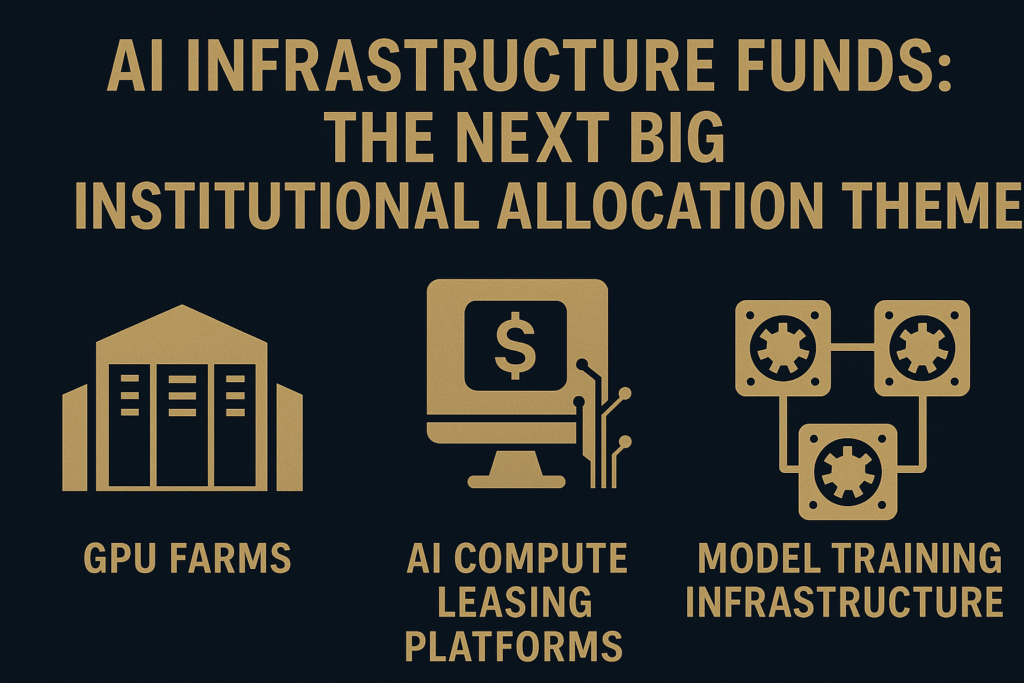

What Exactly Do These Funds Own?

Think of AI infrastructure as a layered ecosystem. Capital can be deployed across three main segments:

1. GPU Farms

These are facilities loaded with thousands of high-performance AI chips. They look like data centers – but with cooling and power configurations tailored specifically to AI workloads.

Investors earn returns as these GPUs are leased out to model developers, startups, cloud providers, and enterprises.

2. AI Compute Leasing Platforms

These are marketplaces where customers can rent compute capacity by the hour or by the project.

Funds investing in leasing platforms benefit from:

– Capacity utilization

– Price per compute unit

– Long-term contracts with enterprises

This is the heart of the “real yield” story – recurring revenue from compute rentals, not speculative growth assumptions.

3. Model Training Infrastructure

Training large models requires vast clusters of interconnected GPUs, high-speed networking, and specialized storage systems. These environments command premium leasing rates because only a handful of companies can build them.

As demand for training new foundation models accelerates worldwide, this infrastructure becomes even more valuable.

The Real Yield Story: Why Investors Love Compute Leasing

Traditional yield assets (like real estate or bonds) face structural pressure: low returns, inflation risk, and limited growth.

AI compute leasing is different.

Real, Contract-Backed Cash Flow

Leasing agreements often span months or years, and the tenants (AI developers, cloud platforms, government labs) are typically well-capitalized.

Scarcity Premium

High-end GPUs like NVIDIA’s H100s and B200s are still supply-constrained. Scarcity pushes up utilization rates – and leasing prices.

Rapid Payback Periods

Some AI infrastructure funds report hardware payback timelines measured in 12–24 months, depending on utilization. After that, the asset continues generating cash flow.

Tech Cycle Tailwinds

Even as chip generations improve, demand consistently outpaces supply. Older GPU clusters can still be monetized for inference, fine-tuning, or smaller models.

In other words: returns are real, recurring, and driven by global AI demand – not hype.

The Demand Explosion: Why This Theme Has “Supercycle” Potential

The world is racing to build AI capacity. Three forces are driving exponential demand:

1. Enterprises are adopting AI at scale

Banks, healthcare providers, manufacturers, and retailers are all running more AI workloads every quarter. Many prefer leasing compute rather than building expensive infrastructure themselves.

2. Governments want sovereign AI capabilities

Countries are funding national compute clusters to ensure independence from private cloud providers.

3. Model innovation requires more compute with every generation

Training runs that cost $10 million two years ago may cost $100 million or more today. Every improvement in model architecture increases compute needs.

This isn’t cyclical demand – it’s structural. It’s the digital equivalent of the early oil boom.

Why Institutions Are Moving Now

Institutional allocators see a rare window:

– A new alternative asset class with real yield

– A multi-decade demand curve

– Hard assets backed by global supply constraints

– An early-cycle opportunity similar to early cloud or telecom infrastructure

As a result, new AI infrastructure funds are raising billions. Many have waiting lists.

This is quickly becoming one of the next major institutional allocation themes, comparable to the emergence of private credit or renewable infrastructure over the last decade.

Risks and Considerations

No asset class is without risk. Key factors to evaluate include:

– Hardware depreciation: mitigated by strong secondary markets

– Utilization risk: reduced with long-term contracts

– Power & cooling costs: especially for large GPU clusters

– Regulatory considerations: national AI policies may change leasing dynamics

A strong fund manager focuses on:

– Data center quality

– Chip procurement relationships

– Long-term customer contracts

– Flexible redeployment strategies

Conclusion: AI Infrastructure Funds Are the New Frontier of Real Yield

AI isn’t just changing technology – it’s changing investment portfolios.

For institutions seeking stable income, exposure to hard assets, and alignment with one of the most powerful technology revolutions of our time, AI infrastructure funds offer a compelling opportunity.

With global compute demand growing exponentially, GPU farms, compute leasing platforms, and model training infrastructure may become the backbone of a new alternative asset class – one built on real yield, real scarcity, and real long-term demand.