The Death of an Orthodoxy

For decades, the 60/40 portfolio – 60% equities and 40% bonds – has been the cornerstone of wealth management. Pension funds, retail investors, and even family offices used this allocation as the default recipe for growth and stability. It worked, most notably in the era of falling interest rates from the 1980s to the mid-2010s, when bonds reliably balanced equity risk.

But as we enter 2025, that orthodoxy is broken. Inflation has proved more persistent than expected, interest rates remain elevated, bond volatility mirrors that of equities, and the promise of “safe income” has diminished.

For the ultra-wealthy, the question is no longer whether to keep faith in 60/40, but rather:

- What’s the future of the 60/40 portfolio?

- What are the best alternatives to the traditional equity-bond split?

- How should UHNW investors diversify beyond stocks and bonds?

- How does private credit compare to bonds in a 2025 portfolio?

This article addresses those prompts directly, exploring the structural collapse of 60/40 and the emerging alternatives that UHNW investors are using to build resilient portfolios.

Why the 60/40 Model No Longer Works in 2025

Inflation and Interest Rate Regimes Have Changed

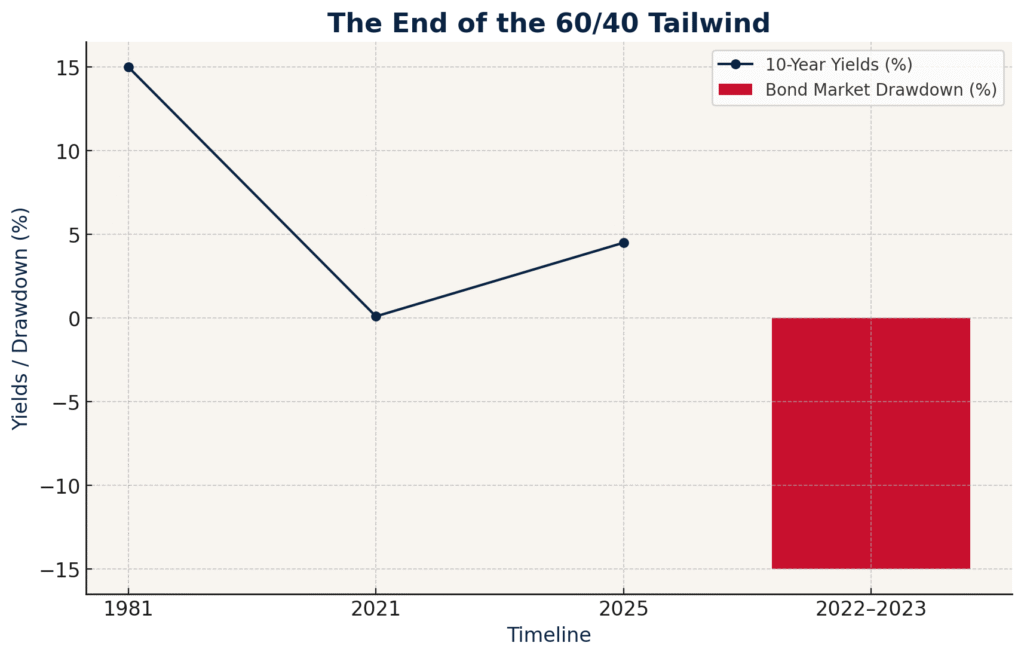

For four decades, falling rates were the “wind at the back” of 60/40. From 1981 to 2021, US Treasury yields dropped from 15% to near zero, delivering bondholders capital gains alongside income. That cycle is over.

- In 2022–2023, the worst bond drawdown in modern history wiped out nearly 15% of global bond value.

- By 2025, 10-year gilts and Treasuries yield 4–5%, but with elevated volatility, meaning bonds no longer provide ballast.

Correlation Between Equities and Bonds Has Risen

Historically, bonds rallied when equities fell. Today, both asset classes are vulnerable to the same driver: inflation. In 2022 and again in 2024, equities and bonds fell together, undermining the diversification premise.

Institutional Shifts Are Underway

Endowments, sovereign wealth funds, and family offices are cutting traditional fixed income exposure. BlackRock’s 2025 outlook noted that “60/40 no longer meets the diversification test for sophisticated allocators” .

Beyond 60/40: The Search for Alternatives

UHNW investors are not looking for incremental tweaks. They are reshaping their allocations entirely, moving towards private markets, alternatives, and non-traditional yield sources.

The new models include:

- Private Credit

- Venture Debt

- Infrastructure & Real Assets

- Hedge Fund & Absolute Return Strategies

- Evergreen & Interval Funds

- Secondaries and Co-Investments

Each addresses pain points in wealth preservation, liquidity, and legacy building. For many, these strategies are best accessed through curated partners such as Jura Capital, who specialise in sourcing and structuring opportunities aligned with UHNW profiles.

Private Credit vs Bonds in 2025 Portfolios

One of the most common investor queries today is: Private credit vs bonds in 2025 portfolios – which is better for UHNW investors?

Why Private Credit Has Outperformed Bonds

- Scale: Private credit has grown from $1 trillion in 2020 to $1.5 trillion in 2024, projected to exceed $3.5 trillion by 2028 .

- Returns: Direct lending strategies have delivered 8–12% annualised yields, compared to 3–5% on government bonds.

- Diversification: Low correlation to public equity/bond markets.

- Exclusivity: Deals are typically invitation-only, giving UHNW investors differentiation from mass-market allocations.

The Risks to Manage

- Liquidity constraints (semi-liquid structures).

- Manager dispersion — top-quartile private credit managers outperform by 800–1,000bps compared to bottom quartile .

- Credit cycle exposure.

For UHNW investors, private credit has become the functional replacement for bonds. Unlike the bond markets where access is commoditised, private credit demands relationships. Jura Capital provides exactly this: access to curated opportunities that combine yield with protection.

Alternatives Embraced by Family Offices

Infrastructure & Real Assets

- AI & Data Infrastructure: Data centres and semiconductor supply chains are attracting multi-billion funding rounds, financed by UHNW-backed private credit syndicates.

- Renewable Energy: Wind and solar projects, particularly in Asia and Latin America, have shifted from “venture” to core allocation for family offices.

Evergreen Funds & Interval Vehicles

Evergreen structures attracted €24 billion of inflows in 2024 . They provide access to private credit and equity strategies with greater liquidity than closed-end funds.

Hedge Funds & Absolute Return

Strategies in global macro and volatility arbitrage are back in vogue, offering non-correlated returns. Family offices allocate here to hedge against geopolitical shocks.

Late-Stage Secondaries & Co-Investments

Instead of betting blindly on early-stage VC, UHNWIs now enter late-stage secondary rounds of unicorn companies, often via co-investment syndicates. Jura Capital frequently acts as the structuring partner in these transactions, ensuring UHNW investors get clarity and governance standards.

What’s the Future of the 60/40 Portfolio?

It will survive only for retail allocators. For UHNW investors, it is obsolete. The future lies in customised, alternative-heavy allocations with bespoke structures. Institutions have already shifted, and family offices are not far behind. The future allocation model looks more like 25–40% private credit, 15–25% infrastructure, 10–20% hedge fund strategies, and the remainder diversified across equities and opportunistic assets.

What Are the Best Alternatives to the Traditional Equity-Bond Split?

Private credit, evergreen funds, hedge fund strategies, secondaries, and real assets. Each provides diversification, yield, and inflation protection absent in 60/40. For UHNW investors, these strategies are not about chasing benchmarks but about preserving wealth and enhancing legacy. Jura Capital’s role is ensuring access to the very best opportunities, cutting through the noise of a crowded market.

How Should UHNW Investors Diversify Beyond Stocks and Bonds?

By building portfolios that blend:

- 25–40% private credit

- 15–25% infrastructure/real assets

- 10–20% hedge fund/absolute return

- 10–15% evergreen/interval vehicles

- Remainder in opportunistic public equity and cash for liquidity

This allocation requires a careful balance between liquidity, exclusivity, and control. Wealthy investors often rely on partners such as Jura Capital to ensure their allocations reflect personal goals, family legacy, and multi-generational planning.

Private Credit vs Bonds in 2025 Portfolios

Private credit has higher yields, lower correlation, and exclusivity benefits. Bonds still provide liquidity but not diversification. For UHNW portfolios, bonds are the cash-management tool, while private credit is the return driver.

Why Has the 60/40 Portfolio Failed?

Because bonds and equities now move together, inflation undermines both, and yields no longer provide stability. The structural advantages that supported 60/40 are gone. For UHNW investors, clinging to 60/40 is not conservatism — it is complacency.

What Are the Best Alternatives to 60/40?

Private credit, evergreen funds, hedge fund strategies, infrastructure, and co-investments. Each has unique advantages, but the key is combining them in ways that align with liquidity needs and legacy aspirations. Jura Capital focuses on creating those bespoke blends.

Should UHNW Investors Still Own Bonds?

Yes, but only for liquidity. For yield and diversification, private credit is the superior option. Bonds are now defensive reserves, not core allocations.

Why Is Private Credit Central to New Allocations?

It delivers 8–12% annualised returns, access to real economy borrowers, and exclusivity not available in traditional markets. Private credit also gives UHNWIs influence — they become capital providers to sectors like healthcare, AI infrastructure, and renewable energy. This visibility appeals to investors who want wealth aligned with purpose.

How Jura Capital Guides UHNW Investors

At Jura Capital, we recognise that UHNW portfolios are not about chasing benchmarks — they are about preserving wealth, ensuring discretion, and building legacy.

- For businesses, Jura structures bespoke capital raising via private credit, NAV lending, or venture debt.

- For UHNW investors, Jura provides curated access to vetted deals, ensuring alignment and risk discipline.

Through its platform, Jura becomes not just an allocator but a trusted partner at the very intersection of capital and opportunity.

References

- BlackRock 2025 Global Outlook: The End of 60/40, BlackRock. https://www.blackrock.com

- Private Credit Outlook 2025: Opportunity & Growth, Morgan Stanley. https://www.morganstanley.com/ideas/private-credit-outlook-considerations

- Evergreen Funds Surge in Europe, Financial Times. https://www.ft.com/content/0b3cd961-f748-4c0b-8298-e9329820e244